| Spouse 1

Age |

Beginning

Portfolio Balance |

Annual

Interest Earnings |

Savings

before Retirement |

Other

Incomes |

Social

Security |

Retirement

Spending |

Income

Tax |

Portfolio

Withdrawal |

Ending

Balance |

Capital

Gain Taxes |

Total Money

Available for Spending |

|---|

SUPPLEMENTAL MATERIAL

In this table, it is assumed that all values are at today’s date, so if Spouse 1’s next birthday is in 0.57 year, for example, then the first-row values are normalized for the next birthday in 0.57 year using financial formulas.

Annual Interest Earnings

The interest used to calculate earnings comes from the type of investment selected, Conservative, Moderate, and Aggressive. Users can change these percentages.

Savings Before Retirement

These are the amounts that users are saving from their salaries while still working. When both spouses retire, there are no more savings and the savings are added to the IRA1 accounts.

Other Incomes

Other Incomes (Pensions and Annuities) start appearing when the person retires.

Social Security

Social Security benefits start at the age when the user starts collecting Social Security, and it increases using the cost-of-living average for the last ten years.

Retirement Spending

It starts when Spouse 1 retires. The annual value depends on the selected “Retirement Spending Strategy”.

Income Tax

This is the Federal Income tax after retirement.

Portfolio Withdrawal

Depends on the “Type of Portfolio Withdrawal Strategy” selected.

If the withdrawal strategy is “Pre-Retirement Spending,” then,

Portfolio Withdrawal = Retirement Spending – Other Incomes – Social Security.

Both lines, Portfolio Withdrawal and Retirement Spending, will be the same.

Ending Balance

Portfolio Balance at the End of the Year = Portfolio Balance at the Beginning of the Year + Annual Interest Earnings + Savings before Retirement – Portfolio Withdrawal - Taxes.

Total Money Available for Spending

Equal to Social Security Benefits + Other Incomes (Pension and Annuities) + Portfolio Withdrawals.

| Age | Taxable

Account Balance |

Non-Taxable

(IRA, 401K) Account 1 Balance |

Non-Taxable

(IRA, 401K) Account 2 Balance |

Non-Taxable

(IRA, 401K) Account 3 Balance |

IRS

RMD Percentage |

IRS RMD

for IRA Account 1 |

IRS RMD

for IRA Account 2 |

IRS RMD

for IRA Account 3 |

Taxable

Account Withdraw |

IRA

Account 1 Withdraw |

IRA

Account 2 Withdraw |

IRA

Account 3 Withdraw |

|---|

SUPPLEMENTAL MATERIAL

This table is divided into three sections.

Left Section

Shows the balance of each of the three accounts over time. In this tool, withdrawals are made first from the Taxable Account (non-IRA account), until it is exhausted. Then, withdrawals begin from the Non-Taxable (IRA, 401K) Account 1, until it is exhausted; then from the next Non-Taxable (IRA, 401K) Account 2, and so on.

Center Section

The IRS requires that individuals who have attained age 72 make a minimum withdrawal of a specified percentage of their pension (IRA and 401(k)) wealth balance on the previous 31st of December, based on age-varying percentages; then, most importantly, taxes on those withdrawals must be paid. These withdrawals are called Minimum Required Distributions (RMD) and are based on the IRS’s life expectancy factors for different ages. The RMD percentage is equal to 1 / (IRS Life Expectancy Factor).

This section shows the RMD amounts required by the IRA to be withdrawn over time.

The IRS uses two tables to determine the life expectancy factors.

- The Joint Life Expectancy, Table II is for IRA owners whose spouses are more than 10 years younger. The life expectancy value is different based on the spouses’ age differences.

- The Uniform Lifetime Table III is for IRA owners whose spouses are not more than 10 years younger. In the IRS life expectancy calculation, the hypothetical spouse is assumed to be exactly 10 years younger even if she (or he) is the same age or older than the primary retiree.

The ages of Spouse 1 and Spouse 2 are their ages on their birthdays in each specific year. Using the Joint Life Expectancy Table II will result in a smaller RMD than using the Uniform Lifetime Table III.

Right Section

This section shows the withdrawals from all accounts.

In this tool, for every year after 72, the total RMDs from all accounts are withdrawn from one of the Non-Taxable (IRA, 401K) accounts. Regardless of the Withdrawal Strategy selected, the total RMDs from all accounts are always withdrawn. If the total RMD amount required to withdraw by the IRS is higher than the money that you need to withdraw according to the Withdrawal Strategy, then, the difference is moved to the taxable, non-IRA account.

It could be that your expenses exhaust the Taxable Account, the non-IRA account of your portfolio, and you will need to withdraw from your IRA accounts before you are 72-years-old.

Excerpts from IRS Publication 590-B, Distributions from Individual Retirement Arrangements

https://www.irs.gov/pub/irs-pdf/p590b.pdf

When Can You Withdraw or Use Assets? You can withdraw or use your traditional IRA assets at any time. However, a 10% additional tax generally applies if you withdraw or use IRA assets before you reach age 59½, which is the minimum age for penalty-free withdrawals.

IRA account balance. The IRA account balance is the amount in the IRA at the end of the year preceding the year for which the required minimum distribution is being figured.

Distributions by the required beginning date. Even if you begin receiving distributions before you reach age 70½, you must begin calculating and receiving required minimum distributions by your required beginning date.

More than minimum received. If in any year, you receive more than the required minimum distribution for that year, you will not receive credit for the additional amount when determining the minimum required distributions for future years. This does not mean that you do not reduce your IRA account balance. It means that if you receive more than your required minimum distribution in one year, you cannot treat the excess (the amount that is more than the required minimum distribution) as part of your required minimum distribution for any later year. However, any amount distributed in your 70½ year will be credited toward the amount that must be distributed by April 1 of the following year.

More than one IRA. If you have more than one traditional IRA, you must determine a separate required minimum distribution for each IRA. However, you can total these minimum amounts and take the total from any one or more of the IRAs.

Figure 1 - Portfolio over Time

Figure 2 – Retirees Wealth over Time

Figure 3 – Account Balances over Time

Figure 4 – Normalized Savings, Probability of Survival, and Probability of Secure Retirement

Figure 5 – Longevity & Remaining Life Expectancy Statistics for 65-Year-Olds

SUPPLEMENTAL MATERIAL

Portfolio value increases from today’s date until retirement. Then, depending on the expenses and accumulated savings, the portfolio increases or decreases.

Play “What if” by changing inputs to achieve your goals, for example, that your money will last at least until you die.

Total Money Available for Spending = Social Security Benefits + Other Incomes (Pension and Annuities) + Portfolio Withdrawals.

The first goal is to have, year after year, money available to pay for your standard of living after retirement, i.e., for retirement spending.

The second goal is to have some extra money available between the ages of 65 to 75, ages when you’re more likely to be able to enjoy possibilities for travel and other leisure activities.

Figure 1 - Portfolio over Time

This chart is a good reference to visualize how your portfolio changes before and after retirement and to see how long your money will last. Regardless of how long your money will last, the question is, will you be able to withdraw enough money from your portfolio to pay for your standard of living at retirement? See Figure 2.

Figure 2 – Retirees Wealth over Time

This chart shows Social Security, Other Incomes (pensions and annuities), Retirement Spending (Standard of Living), Portfolio Withdrawals, and Money Available for Spending.

Do you have enough money available, year after year, to pay for your retirement expenses, in other words, to sustain the standard of living that you selected? In this chart, if the line “Total Money Available for Spending,” is directly over the line, “Retirement Spending,” it means that you do. If not, it means that you do not have enough money to pay for your retirement spending. Therefore, you need to increase your withdrawals amount by changing your withdrawal strategy, to 6% for example, or by reducing your standard of living expenses.

Total Money Available for Spending = Social Security + Other Incomes + Portfolio Withdrawals

The portfolio withdrawals depend on the withdrawal strategy selected. If you want to withdraw from your portfolio exactly the amount of money that you need to supplement your retirement income to be able to sustain the standard of living that you want, then the easiest way is to select Pre-Retirement Spending as your retirement strategy. The tool will calculate how much money is required to be withdrawn from your savings to pay for your inflation-adjusted spending (standard of living) plus taxes by calculating the following:

Portfolio Withdrawals = Expenses – Social Security – Pensions - Annuities

When the Pre-Retirement Spending strategy is selected, the lines, Total Money Available for Spending and “Retirement Spending,” appear one on top of the other because their values are the same.

Figure 3 – Account Balances over Time

Figure 3 shows the balance of each account, Non-IRA, IRA1, IRA2, and IRA3 over time, and how they are depleted or how they increase.

Figure 4 – Savings Depletion and Survival Probability

Show Savings Depletion over time after retirement and Gompertz - Makeham Probability of Survival (tPx). The Probability of Survival is the probability that someone aged exactly x will survive for t more years, i.e. live up to at least age x + t years. At retirement age, x, the probability of survival is 100%, and then it starts decreasing to around 2.5% at 100 when t = 100 – retirement age.

| Enter Age Markers for Snapshot |

|---|

Summary Information

| Age | |||||

|---|---|---|---|---|---|

| Social Security | |||||

| Other Incomes | |||||

| Total Portfolio Withdrawal | |||||

| Total Money Available for Spending | |||||

| Retirement Spending | |||||

| Money for Extra Spending | |||||

| Portfolio Ending Balance | |||||

| Standard of Living Risk (No risk if value is >=0) |

Account Values at the End of the Year

| Age | |||||

|---|---|---|---|---|---|

| Non-IRA Account | |||||

| IRA Account 1 | |||||

| IRA Account 2 | |||||

| IRA Account 3 | |||||

| Total |

Account Withdraws at the End of the Year

| Age | |||||

|---|---|---|---|---|---|

| Non-IRA Account | |||||

| IRA Account 1 | |||||

| IRA Account 2 | |||||

| IRA Account 3 | |||||

| Total |

IRS Required Minimum Distributions (RMDs)

| Age | |||||

|---|---|---|---|---|---|

| RMD Percentage | |||||

| IRA Account 1 | |||||

| IRA Account 2 | |||||

| IRA Account 3 | |||||

| Total |

Tax Calculations

| Age | |||||

|---|---|---|---|---|---|

| Spouse 1 Social Security benefits | |||||

| Spouse 2 Social Security benefits | |||||

| Total Social Security - Line 1 | |||||

| One half of line #1 - Line 2 | |||||

| Adjusted Gross Income - Line 3 | |||||

| Provisional Income (Add Lines 2 and 3) - Line 4 | |||||

| Taxable Social Security Benefit - Line 5 | |||||

| Total Income (Add lines 3 and 5) - Line 6 | |||||

| Taxable Income | |||||

| Income Taxes |

SUPPLEMENTAL MATERIAL

Snapshots provide quick and easy access to a portfolio and show the state of the portfolio at five markers in time, certain selected ages of Spouse 1.

As a detailed table of contents that provides the user with accessible information of data, a Snapshot can be used to verify the state of the user’s portfolio at particular ages.

The default markers are the ages of 70, 75, 80, 85, and 90, but they can be changed at the top.

The Snapshot provides the following information in five different sections:

- Summary Information

- Account Values at the End of the Year

- Account Withdraws also at the End of the Year

- IRS Required Minimum Distributions (RMDs)

- Tax Calculations

The Standard of Living Risk (SLR) is the risk that the current or a specified acceptable lifestyle may not be sustainable. In this tool, Retirement Spending, Life Style, and Standard of Living are used interchangeably.

As long as the “Total Money Available for Spending” is higher than the “Retirement Spending,” there is no “Standard of Living Risk.”

Required Minimum Distribution

The Required Minimum Distribution (RMD) is calculated by multiplying the end of the previous year IRA Account value times the RMD percentage of the current year. In this tool, the first RMD is taken on Spouses’ 70th birthday year, regardless of when the Spouse turn 70½.

Income Tax Calculations

The income Tax calculation follows Pub 915, line per line, to calculate the Taxable Social Security Benefits. In this tool, the Adjusted Gross Income is equal to IRA accounts withdrawals + Other Incomes after Retirement. Then, the current standard deductions and personal tax exemptions are deducted (Lines 8 and 9 of the Form 1040) to calculate the Taxable Income, line10. The current tax brackets are applied to the Taxable Income to calculate the Total Income Tax.

MONTE CARLO SIMULATION

A Monte Carlo simulation analyzes the likelihood of a portfolio being successful by randomizing certain factors and checking the annual result at certain points called percentiles. In this tool, two factors change at random for the simulation, the rate of return and inflation. Then, the simulation is run a 500 times each year and the percentiles are plotted on a graph.

When users select a type of investment, Conservative, Moderate, or Aggressive, they are selecting the rate of return for their investment. In this tool, that rate of return is used before and after retirement; it doesn’t change because it is impossible to know for sure the rate of return for next year, much less for 20 years from now. In this tool, the Monte Carlo simulation shows the interest per year change at random (using the invert of the normal distribution).

The chart shows the percentiles at 25%, 50%, and 75%. A 25% percentile means that there is only a 25% chance that the balance of a portfolio will be below and the remaining 75% that the portfolio balance will be better.

| Age | 25th Pctile | 50th Pctile | 75th Pctile |

|---|

Please Wait

LONGEVITY SIMULATION

Summary Information

| Remaining Lifetime | |||||

| Longevity | |||||

| Probability of Survival |

Figure 5 – Remaining Lifetime - RP-2012 (Improved 2018)

Figure 6 – Life Expectancy - RP-2012 (Improved 2018)

Longevity & Remaining Lifetime Tool

Age and Mortality

What is your remaining lifetime? If you know that you will die before 75, then you will spend more of your retirement, but what about if you live to 95? Maybe you need to spend less. Also, what about if you are living with another person and would like your savings to last one of you, longest survival, then, the length of retirement in your calculations should be longer.

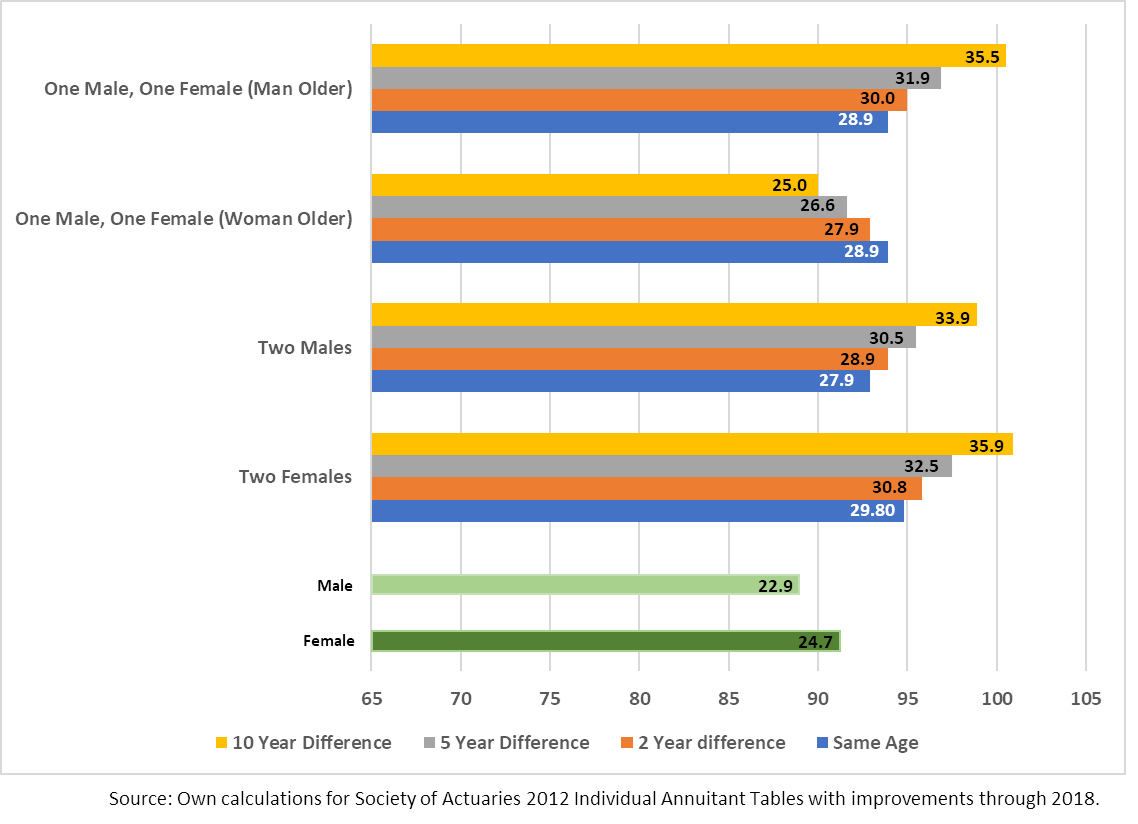

Retirees should look first at the Remaining Life Expectancy at age x, which shows, statistically, how many more years people are going to live, as an individual or as a couple, so they can plan their retirement. There are several factors to consider in this calculation: (1) Single or couple; (2) Gender; (3) Life Expectancy for the couple’s longest survivor: (4) Combination of couple’s genders, i.e., one male-one female, two males, two females); (5) Couple’s age difference.

If you are single or do not wish to use the joint-life expectancy features in the program, leave the “Spouse 2” entry as (Select) and only enter your gender under, “Spouse 1.” For your spouse/partner, enter the gender in the “Spouse 2” column and the age difference between Spouse 1 and Spouse 2.

If you want the chart to start at an age other than 65, enter that age in “Chart Starting Age”; otherwise leave that blank and the illustrations will start at 65.

You don’t need to enter information in Steps 1 – 9 to use the Longevity & Remaining Lifetime calculator. You can always come back and play, “What If”, and see how the results change when you enter different Genders and Couple’s Age Gap.

Snapshots provide quick and easy access to the calculations, as well as showing the Remaining Lifetime and Longevity information at five markers in time, certain selected ages of Spouse 1. The default markers are the ages of 65, 70, 75, 80, and 85, but they can be changed at the top.

How the calculations are done?

There are several tables to model human mortality, among them being those from the Social Security Agency, the IRS, the Society of Actuaries, and the Gompertz-Makeham law of mortality. The starting point is qx, the probability of dying between ages x and x + 1; from there, it is possible to calculate the Remaining Life Expectancy, the Longevity at age x, and the Probability of Survival (xPt), the probability that a person at age x will die within the next x + t years.

The Longevity and Remaining Lifetime calculator uses the Society of Actuaries, 2012, Individual Annuity Mortality IAR Table. Note that the Society of Actuaries table shows individuals living about four to five years longer than the Social Security life table and the Society of Actuaries data.

The Society of Actuaries 2012 table is a “generational” mortality table, in which qx can be recalculated for years after 2012 using the following formula:

qx2012+n = qx2012 (1 – G2x)n

where n is the projection year minus 2012. The projection year for the calculation of Longevity and Remaining Lifetime is 2018, so, n is equal to 6 (2018 – 2012).

CONSUMPTION SMOOTHING DURING RETIREMENT

Calculated

| Age | No. of Years | Optimal

Consumption |

Optimal

Portfolio Withdrawal |

Financial

Capital |

|---|

Figure 7 – Consumption Smoothing

SUPPLEMENTAL MATERIAL

There are several factors involved in the calculation of optimal consumption once retirees stop working; there is no more Human Capital, and then they must live on their retirement incomes and savings. The most important factor is how long the portfolio needs to last –also called Wealth Depletion Time (WDT).

There are two ways to determine the WDT, either by calculating it, or for the retiree to decide what the WDT will be. Moshe Milevsky and Huaxiong Huang developed an algorithm, Patent No. US 8,781,937 B2, to find the Wealth Depletion Time (WDT) to calculate the optimal portfolio withdrawal. In this Consumption Smoothing tool, the selected age in “Living until Age (Death Age)” indicates that the retirees are assuming that they will die at that age, and that they want that age to be their wealth depletion time, i.e., that their savings will be depleted by that age. Now, if they live longer, then they will have to live on just their retirement income (pension, Social Security benefits and annuities income).

Another two factors that influence the optimal withdrawal amount are the following: (1) λ, which captures the component of the death rate that is attributable to accidents and (2) ϒ, the coefficient of relative longevity risk aversion (CRRA).

λ captures the component of the death rate that is attributable to accidents. In practice, λ tends to have a very small value. People who select a value of zero for λ believe that their life is not prone to accidents and, therefore, their Consumption Smoothing will be the same over all their life. People who select a value different than zero think that they may die early in life and, therefore, would like to consume more in their early retirement days.

ϒ, the Constant Relative Longevity Risk Aversion (CRRA), is the “fear” of living longer than determined by actuarial mortality rates, and possibly depleting one's financial resources before dying. ϒ is a number from 1 to 8, negative or positive, but different than zero. The rate of wealth decline is higher and faster for lower CRRAs. Retirees with CRRA (ϒ) = 1 assume that their life expectancy is low, and they don't worry about consuming more in their early retirement days.

- Retirees with CRRA (ϒ) = 1 assume that their life expectancy will be 25 (24.6) years after 65

- Retirees with CRRA (ϒ) = 2 assume that their life expectancy will be 30 (29.6) years after 65

- Retirees with CRRA (ϒ) = 4 assume that their life expectancy will be 35 (34.9) years after 65

- Retirees with CRRA (ϒ) = 8 assume that their life expectancy will be 40 (40.5) years after 65

λ and ϒ are pulling the optimal consumption in different directions. When λ is higher, the retiree will consume more in their early retirement days, and when ϒ is higher, the retiree will consume less in their early retirement days.

One more factor that needs some explanation is the Subjective Rate. If anyone offers someone $100 today or $150 in a year, they most probably will select $150 in a year because they don’t have a way to invest the $100 at a rate of return of 50%. If they are offered $100 today or $101 in a year, they will most probably select $100 today because the interest rate they can earn on their savings is higher than 1%. Now what will be the minimum dollar value that will make you wait for a year? Subjective Rate is the minimum interest rate, r, at which you prefer $100 x (1 + r) in a year instead of $100 today. To the extent that people prefer to get their money today instead of in the future, the Subjective Rate will have to be a little bit higher than the rate of return people will earn on their savings. The Euler equation for consumption explains how interest rate and subjective rate are closely related.

The formulas on pages 298 and 299 from the book, Strategic Financial Planning Over the Life Cycle, (Charupat, Huaxion and Milevsky), have been used, with permission of the authors, to calculate the Consumption Smoothing during retirement in CheckYourretirement.com.

CONTACT INFORMATION

Please use the form below to contact us regarding any question about this tool or with suggestions on how to improve it. You can also email us at admin@checkyourretirments.comDemo & Tutorials

Tool Demo with Pre-Set Financial Data

The best way to become familiar with the tool is to enter pre-set financial data and see how the tool calculates, presents, and plots the information that you enter. Click on Run Demo below and the tool will automatically enter some financial data.

Play the What If game. How many years will my portfolio last if my annual expenses increase to $75,000? What about if the expenses are reduced to $60,000?

If you are a numbers person, click on Portfolio Analysis, Table, and as you are playing “What If,” you will see how the table changes. If you are a visual person, click on Charts and you will see how the charts change as you modify your information.

Run Monte Carlo simulations, When to Start Social Security simulation, or print a Report.

When you feel confident using the tool, then enter your own finance numbers.

Tutorials

Tutorial Part 1: This tutorial provides basic information about how to enter your information and then look up and analyze your results on the “Check Your Retirement” online tool.

TAXES

Income Taxes

For tax purposes, IRA distributions are considered ordinary income. The amount of IRA distribution is added to other sources of income determined to be the adjusted gross income. They will be taxed at the applicable individual federal income tax rate and may also be subject to state and local taxes. There are several papers discussing, for tax efficiency purposes, how to withdraw from savings accounts, but they are too complicated to implement in this tool.

Taxable Social Security Benefits

IRS Publication 915, “Social Security and Equivalent Railroad Retirement Benefits,” page 9, is used, step-by-step, to calculate the taxable SS benefits. All 19 steps in this form are used in the tool to calculate the taxable SS benefit. This is line 5a of IRS Form 1040.

Other Income

Other Incomes After Retirement (Pension, Annuity) and Total IRA Account Withdrawals are added. For tax purposes, IRA withdrawals are considered ordinary income.

Total Income

The Taxable Social Security Benefits and the Total Taxable Income are added to calculate the Total Income. This is line 6 of IRS Form 1040.

Deductions (2019)

If both dates of birth for Spouse 1 and 2 are entered, the tool deducts a Standard Deduction of $12,600 for Married Filing Jointly. If a date of birth for Spouse 2 is not entered, or if the Spouse 2 box is not checked, the tool deducts a Standard Deduction of $6,300 for a Single person. Personal exemptions stay at $4,050 for filers and their dependents. These are the deductions on Line 8 of the IRS Form 1040 respectively.

Taxable Income (Line 10 of IRS Form 1040)

The Total Income minus the Deductions is the Taxable Income.

Tax Brackets

The following IRS 2019 tax brackets are used in the tool to calculate income taxes.

Married Filing Jointly

| Taxable Income | But not over | The tax is | Plus | Of the amount over |

|---|---|---|---|---|

| $0 |

$19,400

|

$0

|

10.0%

|

$0

|

|

$19,401

|

$78,950

|

$1,905

|

12.0%

|

$19,400

|

|

$78,951

|

$168,400

|

$8,907

|

22.0%

|

$78,950

|

|

$168,401

|

$321,450

|

$28,179

|

24.0%

|

$168,450

|

|

$321,451

|

$408,200

|

$64,179

|

32.0%

|

$321,450

|

|

$408,201

|

$612,350

|

$91,379

|

35.0%

|

$408,200

|

|

$612,351

|

$5,000,000

|

$161,379

|

37.6%

|

$612,350

|

Single

| Over | But not over | The tax is | Plus | of the amount over |

|---|---|---|---|---|

|

$0

|

$9,700

|

|

10.0%

|

$0

|

|

$9,701

|

$39,475

|

$953

|

12.0%

|

$9,700

|

|

$39,476

|

$84,200

|

$4,454

|

22.0%

|

$39,475

|

|

$84,201

|

$160,725

|

$14,090

|

24.0%

|

$84,200

|

|

$160,726

|

$204,100

|

$32,090

|

32.0%

|

$160,725

|

|

$204,101

|

$510,300

|

$45,690

|

35.0%

|

$204,100

|

|

$510,301

|

$5,000,000

|

$150690

|

37.6%

|

$510,300

|

Remember that this year you pay the previous year’s taxes. For example, the RMD at age 70 taxes is paid at age 71.

Taxable Social Security Benefits - IRS Publication 915, Social Security and Equivalent Railroad Retirement Benefits, page 9: https://www.irs.gov/pub/irs-pdf/p915.pdf

Capital Gain Taxes

Similarly, Capital Gain tax calculations are also done per IRS guidelines.

- Taxable Account Withdrawal – Withdrawals from taxable (Non-IRA) accounts do not require payment of income taxes, but they do require payment of Capital Gains taxes. When you sell a capital asset, in this case, stocks or bonds, the difference between the adjusted basis in the asset and the amount you realized from the sale is a capital gain or a capital loss. Capital Gain = Selling Price – Purchasing Price.

- Selling Price in this tool is the Taxable Account withdrawal.

- The Purchasing Price is the value of the Taxable Account Withdrawal at the time of retirement. It is the inverse of the Future Value formula: you know FV, i, and N, find PV

- Capital gains and losses are classified as long-term or short-term. If you hold the asset for more than one year before you dispose of it, your capital gain or loss is long-term. If you hold it one year or less, your capital gain or loss is short-term. In this tool, it is assumed that all your capital gains are long-term.

- Long-Term Capital Gains Tax Bracket - The tax rate on most net capital gains is no higher than 15% for most taxpayers. Capital Gain taxes are based now on the individual's or couple's total taxable income. The following IRS 2019 Capital Gain tax brackets are used in the tool to calculate the taxes.

Married Filing Jointly

| Joint Taxable Income | Capital Gain Bracket |

|---|---|

| $77,200 | 0% |

| $77,201 | 15% |

| $479,001 | 20% |

Single

| Single Taxable Income | Capital Gain Bracket |

|---|---|

| $38,600 | 0% |

| $38,601 | 15% |

| $425,801 | 20% |

Capital Gains Taxes https://www.irs.gov/taxtopics/tc409.html

WHEN TO START SOCIAL SECURITY ?

When you click on the Run Simulation button, the tool answers the following question: “What happens to my portfolio value over time when I change my starting Social Security age? For example, would the year-end balance of my portfolio at 75 years of age go up or down if I start Social Security at 70 instead of 66? The values highlighted in Table 1 show which Social Security starting age provides the highest portfolio value at Spouse 1’s age.

Table 1 – Portfolio Values When Using Different Starting Ages for SS Benefits (62 - 70)

| Portfolio Value at Spouse 1 Age | |||||

|---|---|---|---|---|---|

| SS Age | 70 | 75 | 80 | 85 | 90 |

| 62 | |||||

| 63 | |||||

| 64 | |||||

| 65 | |||||

| 66 | |||||

| 67 | |||||

| 68 | |||||

| 69 | |||||

| 70 | |||||

Figure 1 – Portfolio Values When Using Different Starting Ages for SS Benefits (62 - 70)

How to Decide When to Start Receiving Social Security Benefits?

One of the questions many people ask about Social Security benefits is when would be the best age to start the benefits. The rules from the Social Security Agency are very clear and simple. At your full retirement age (FRA), you receive 100% of your benefits. If you start collecting at an earlier age, your benefits will be reduced by a certain percentage, and if you start later than your FRA, your benefits will be increased by a certain percentage. So, if you were born in or after 1960, your FRA is 67. Benefits at your FRA are used as the reference point, when your benefits will be 100%. if you start your benefits at 62, your benefits will be 70% of your FRA. If you start your benefits at 70, your benefits will be 124% of your FRA.

Many financial advisers look at this question by saying that when someone delays claiming U.S. Social Security benefits for some years after FRA, they are effectively buying an inflation-adjusted advanced-life delayed annuity, with survivor benefits for the spouse. For example, check Social Security: The Best Annuity Money Can Buy, Wade Pfau, Ph.D., CFA, and Life Annuities: An Optimal Product for Retirement Income, Moshe A. Milevsky in References.

Both authors, Pfau and Milevsky, conclude that the Social Security payout rate implied on the “annuity” provided by delaying Social Security far exceeds the rate of return available from real or nominal bonds in today’s environment of ultra-low interest rates. For them, delaying annualization is optimal.

But where do you get the money to pay for the annuity, since you would not be receiving your benefits from age 62 until 70? The answer is that during those eight years, you have to take that money from your portfolio. Between 62 and 70, you will have to withdraw more money from your portfolio to keep up with your standard of living expenses.

When deciding when to start your Social Security benefits, this tool answers the following question: “What happens to my portfolio value over time when I change my starting Social Security age? Would the year-end balance of my portfolio at 75 years old, for example, go up or down if I start Social Security at 70 instead of 66?

In this tool, you can do this manually; after selecting your retirement age, select 62 as the starting age for Social Security, go to Snapshot and find the ending value of your portfolio at different ages in your life, 70, 75, 80, 85, and 90. Then repeat the process but change your starting age to 63, 64, 65, …. and 70. Create a table with all these values and decide when to start receiving Social Security benefits based on at what age in your life you would prefer having more money in your portfolio. Or, you can let the tool do it for you by simple clicking on the Run Simulation button. The graph and table above show the hypothetical value of your portfolio retirement savings at different ages in your life using different starting Social Security ages (62 – 70). Based on what the resulting data show you, you can make the appropriate decision for meeting your goals.

There is a direct relationship between the age at which you retire, i.e., stop working, and when you start Social Security benefits. If you change your retirement age, then run the simulation again, and check the results. It seems that it is usually better to start your social Security benefits the year that you retire.

If you change your inputs, remember also to click on “Run Simulation.” The Report includes the last simulation that you ran, regardless of any change in your inputs.

SS BENEFITS

Table 1 - Principal Percentage Benefits Based on the Year a Person was Born

| Age | -1954 | 1955 | 1956 | 1957 | 1958 | 1959 | 1960 - |

| 62 | 75.000% | 74.167% | 73.333% | 72.500% | 71.667% | 70.833% | 70.000% |

| 63 | 80.000% | 79.167% | 78.333% | 77.500% | 76.667% | 75.833% | 75.000% |

| 64 | 86.667% | 85.556% | 84.444% | 83.333% | 82.222% | 81.111% | 80.000% |

| 65 | 93.333% | 92.222% | 91.111% | 90.000% | 88.889% | 87.778% | 86.667% |

| 66 | 100.000% | 98.889% | 97.778% | 96.667% | 95.556% | 94.444% | 93.333% |

| 67 | 108.000% | 106.667% | 105.333% | 104.000% | 102.667% | 101.333% | 100.000% |

| 68 | 116.000% | 114.667% | 113.333% | 112.000% | 110.667% | 109.333% | 108.000% |

| 69 | 124.000% | 122.667% | 121.333% | 120.000% | 118.667% | 117.333% | 116.000% |

| 70 | 132.000% | 130.667% | 129.333% | 128.000% | 126.667% | 125.333% | 124.000% |

Table 2 - Spouse Benefits Based on the Year a Person was Born

| Age | -1954 | 1955 | 1956 | 1957 | 1958 | 1959 | 1960 - |

| 62 | 35.000% | 34.583% | 34.167% | 33.750% | 33.333% | 32.917% | 32.500% |

| 63 | 37.500% | 37.083% | 36.667% | 36.250% | 35.833% | 35.417% | 35.000% |

| 64 | 41.667% | 40.972% | 40.278% | 39.583% | 38.889% | 38.194% | 37.500% |

| 65 | 45.833% | 45.139% | 44.444% | 43.750% | 43.056% | 42.361% | 41.667% |

| 66 | 50.000% | 49.306% | 48.611% | 47.917% | 47.222% | 46.528% | 45.833% |

| 67 | 54.000% | 53.333% | 52.667% | 52.000% | 51.333% | 50.667% | 50.000% |

| 68 | 58.000% | 57.333% | 56.667% | 56.000% | 55.333% | 54.667% | 54.000% |

| 69 | 62.000% | 61.333% | 60.667% | 60.000% | 59.333% | 58.667% | 58.000% |

| 70 | 66.000% | 65.333% | 64.667% | 64.000% | 63.333% | 62.667% | 62.000% |

Table 3 - Percentages Benefits based on the Year and Month a person was Born

| Month | Age | -1954 | 1955 | 1956 | 1957 | 1958 | 1959 | 1960 - |

| 62.000 | 75.000% | 74.167% | 73.333% | 72.500% | 71.667% | 70.833% | 70.000% | |

| 1 | 62.083 | 75.417% | 74.583% | 73.750% | 72.917% | 72.083% | 71.250% | 70.417% |

| 2 | 62.167 | 75.833% | 75.000% | 74.167% | 73.333% | 72.500% | 71.667% | 70.833% |

| 3 | 62.250 | 76.250% | 75.417% | 74.583% | 73.750% | 72.917% | 72.083% | 71.250% |

| 4 | 62.333 | 76.667% | 75.833% | 75.000% | 74.167% | 73.333% | 72.500% | 71.667% |

| 5 | 62.417 | 77.083% | 76.250% | 75.417% | 74.583% | 73.750% | 72.917% | 72.083% |

| 6 | 62.500 | 77.500% | 76.667% | 75.833% | 75.000% | 74.167% | 73.333% | 72.500% |

| 7 | 62.583 | 77.917% | 77.083% | 76.250% | 75.417% | 74.583% | 73.750% | 72.917% |

| 8 | 62.667 | 78.333% | 77.500% | 76.667% | 75.833% | 75.000% | 74.167% | 73.333% |

| 9 | 62.750 | 78.750% | 77.917% | 77.083% | 76.250% | 75.417% | 74.583% | 73.750% |

| 10 | 62.833 | 79.167% | 78.333% | 77.500% | 76.667% | 75.833% | 75.000% | 74.167% |

| 11 | 62.917 | 79.583% | 78.750% | 77.917% | 77.083% | 76.250% | 75.417% | 74.583% |

| 63.000 | 80.000% | 79.167% | 78.333% | 77.500% | 76.667% | 75.833% | 75.000% | |

| 1 | 63.083 | 80.556% | 79.583% | 78.750% | 77.917% | 77.083% | 76.250% | 75.417% |

| 2 | 63.167 | 81.111% | 80.000% | 79.167% | 78.333% | 77.500% | 76.667% | 75.833% |

| 3 | 63.250 | 81.667% | 80.556% | 79.583% | 78.750% | 77.917% | 77.083% | 76.250% |

| 4 | 63.333 | 82.222% | 81.111% | 80.000% | 79.167% | 78.333% | 77.500% | 76.667% |

| 5 | 63.417 | 82.778% | 81.667% | 80.556% | 79.583% | 78.750% | 77.917% | 77.083% |

| 6 | 63.500 | 83.333% | 82.222% | 81.111% | 80.000% | 79.167% | 78.333% | 77.500% |

| 7 | 63.583 | 83.889% | 82.778% | 81.667% | 80.556% | 79.583% | 78.750% | 77.917% |

| 8 | 63.667 | 84.444% | 83.333% | 82.222% | 81.111% | 80.000% | 79.167% | 78.333% |

| 9 | 63.750 | 85.000% | 83.889% | 82.778% | 81.667% | 80.556% | 79.583% | 78.750% |

| 10 | 63.833 | 85.556% | 84.444% | 83.333% | 82.222% | 81.111% | 80.000% | 79.167% |

| 11 | 63.917 | 86.111% | 85.000% | 83.889% | 82.778% | 81.667% | 80.556% | 79.583% |

| 64.000 | 86.667% | 85.556% | 84.444% | 83.333% | 82.222% | 81.111% | 80.000% | |

| 1 | 64.083 | 87.222% | 86.111% | 85.000% | 83.889% | 82.778% | 81.667% | 80.556% |

| 2 | 64.167 | 87.778% | 86.667% | 85.556% | 84.444% | 83.333% | 82.222% | 81.111% |

| 3 | 64.250 | 88.333% | 87.222% | 86.111% | 85.000% | 83.889% | 82.778% | 81.667% |

| 4 | 64.333 | 88.889% | 87.778% | 86.667% | 85.556% | 84.444% | 83.333% | 82.222% |

| 5 | 64.417 | 89.444% | 88.333% | 87.222% | 86.111% | 85.000% | 83.889% | 82.778% |

| 6 | 64.500 | 90.000% | 88.889% | 87.778% | 86.667% | 85.556% | 84.444% | 83.333% |

| 7 | 64.583 | 90.556% | 89.444% | 88.333% | 87.222% | 86.111% | 85.000% | 83.889% |

| 8 | 64.667 | 91.111% | 90.000% | 88.889% | 87.778% | 86.667% | 85.556% | 84.444% |

| 9 | 64.750 | 91.667% | 90.556% | 89.444% | 88.333% | 87.222% | 86.111% | 85.000% |

| 10 | 64.833 | 92.222% | 91.111% | 90.000% | 88.889% | 87.778% | 86.667% | 85.556% |

| 11 | 64.917 | 92.778% | 91.667% | 90.556% | 89.444% | 88.333% | 87.222% | 86.111% |

| 65.000 | 93.333% | 92.222% | 91.111% | 90.000% | 88.889% | 87.778% | 86.667% | |

| 1 | 65.083 | 93.889% | 92.778% | 91.667% | 90.556% | 89.444% | 88.333% | 87.222% |

| 2 | 65.167 | 94.444% | 93.333% | 92.222% | 91.111% | 90.000% | 88.889% | 87.778% |

| 3 | 65.250 | 95.000% | 93.889% | 92.778% | 91.667% | 90.556% | 89.444% | 88.333% |

| 4 | 65.333 | 95.556% | 94.444% | 93.333% | 92.222% | 91.111% | 90.000% | 88.889% |

| 5 | 65.417 | 96.111% | 95.000% | 93.889% | 92.778% | 91.667% | 90.556% | 89.444% |

| 6 | 65.500 | 96.667% | 95.556% | 94.444% | 93.333% | 92.222% | 91.111% | 90.000% |

| 7 | 65.583 | 97.222% | 96.111% | 95.000% | 93.889% | 92.778% | 91.667% | 90.556% |

| 8 | 65.667 | 97.778% | 96.667% | 95.556% | 94.444% | 93.333% | 92.222% | 91.111% |

| 9 | 65.750 | 98.333% | 97.222% | 96.111% | 95.000% | 93.889% | 92.778% | 91.667% |

| 10 | 65.833 | 98.889% | 97.778% | 96.667% | 95.556% | 94.444% | 93.333% | 92.222% |

| 11 | 65.917 | 99.444% | 98.333% | 97.222% | 96.111% | 95.000% | 93.889% | 92.778% |

| 66.000 | 100.000% | 98.889% | 97.778% | 96.667% | 95.556% | 94.444% | 93.333% | |

| 1 | 66.083 | 100.667% | 99.444% | 98.333% | 97.222% | 96.111% | 95.000% | 93.889% |

| 2 | 66.167 | 101.333% | 100.000% | 98.889% | 97.778% | 96.667% | 95.556% | 94.444% |

| 3 | 66.250 | 102.000% | 100.667% | 99.444% | 98.333% | 97.222% | 96.111% | 95.000% |

| 4 | 66.333 | 102.667% | 101.333% | 100.000% | 98.889% | 97.778% | 96.667% | 95.556% |

| 5 | 66.417 | 103.333% | 102.000% | 100.667% | 99.444% | 98.333% | 97.222% | 96.111% |

| 6 | 66.500 | 104.000% | 102.667% | 101.333% | 100.000% | 98.889% | 97.778% | 96.667% |

| 7 | 66.583 | 104.667% | 103.333% | 102.000% | 100.667% | 99.444% | 98.333% | 97.222% |

| 8 | 66.667 | 105.333% | 104.000% | 102.667% | 101.333% | 100.000% | 98.889% | 97.778% |

| 9 | 66.750 | 106.000% | 104.667% | 103.333% | 102.000% | 100.667% | 99.444% | 98.333% |

| 10 | 66.833 | 106.667% | 105.333% | 104.000% | 102.667% | 101.333% | 100.000% | 98.889% |

| 11 | 66.917 | 107.333% | 106.000% | 104.667% | 103.333% | 102.000% | 100.667% | 99.444% |

| 67.000 | 108.000% | 106.667% | 105.333% | 104.000% | 102.667% | 101.333% | 100.000% | |

| 1 | 67.083 | 108.667% | 107.333% | 106.000% | 104.667% | 103.333% | 102.000% | 100.667% |

| 2 | 67.167 | 109.333% | 108.000% | 106.667% | 105.333% | 104.000% | 102.667% | 101.333% |

| 3 | 67.250 | 110.000% | 108.667% | 107.333% | 106.000% | 104.667% | 103.333% | 102.000% |

| 4 | 67.333 | 110.667% | 109.333% | 108.000% | 106.667% | 105.333% | 104.000% | 102.667% |

| 5 | 67.417 | 111.333% | 110.000% | 108.667% | 107.333% | 106.000% | 104.667% | 103.333% |

| 6 | 67.500 | 112.000% | 110.667% | 109.333% | 108.000% | 106.667% | 105.333% | 104.000% |

| 7 | 67.583 | 112.667% | 111.333% | 110.000% | 108.667% | 107.333% | 106.000% | 104.667% |

| 8 | 67.667 | 113.333% | 112.000% | 110.667% | 109.333% | 108.000% | 106.667% | 105.333% |

| 9 | 67.750 | 114.000% | 112.667% | 111.333% | 110.000% | 108.667% | 107.333% | 106.000% |

| 10 | 67.833 | 114.667% | 113.333% | 112.000% | 110.667% | 109.333% | 108.000% | 106.667% |

| 11 | 67.917 | 115.333% | 114.000% | 112.667% | 111.333% | 110.000% | 108.667% | 107.333% |

| 68.000 | 116.000% | 114.667% | 113.333% | 112.000% | 110.667% | 109.333% | 108.000% | |

| 1 | 68.083 | 116.667% | 115.333% | 114.000% | 112.667% | 111.333% | 110.000% | 108.667% |

| 2 | 68.167 | 117.333% | 116.000% | 114.667% | 113.333% | 112.000% | 110.667% | 109.333% |

| 3 | 68.250 | 118.000% | 116.667% | 115.333% | 114.000% | 112.667% | 111.333% | 110.000% |

| 4 | 68.333 | 118.667% | 117.333% | 116.000% | 114.667% | 113.333% | 112.000% | 110.667% |

| 5 | 68.417 | 119.333% | 118.000% | 116.667% | 115.333% | 114.000% | 112.667% | 111.333% |

| 6 | 68.500 | 120.000% | 118.667% | 117.333% | 116.000% | 114.667% | 113.333% | 112.000% |

| 7 | 68.583 | 120.667% | 119.333% | 118.000% | 116.667% | 115.333% | 114.000% | 112.667% |

| 8 | 68.667 | 121.333% | 120.000% | 118.667% | 117.333% | 116.000% | 114.667% | 113.333% |

| 9 | 68.750 | 122.000% | 120.667% | 119.333% | 118.000% | 116.667% | 115.333% | 114.000% |

| 10 | 68.833 | 122.667% | 121.333% | 120.000% | 118.667% | 117.333% | 116.000% | 114.667% |

| 11 | 68.917 | 123.333% | 122.000% | 120.667% | 119.333% | 118.000% | 116.667% | 115.333% |

| 69.000 | 124.000% | 122.667% | 121.333% | 120.000% | 118.667% | 117.333% | 116.000% | |

| 1 | 69.083 | 124.667% | 123.333% | 122.000% | 120.667% | 119.333% | 118.000% | 116.667% |

| 2 | 69.167 | 125.333% | 124.000% | 122.667% | 121.333% | 120.000% | 118.667% | 117.333% |

| 3 | 69.250 | 126.000% | 124.667% | 123.333% | 122.000% | 120.667% | 119.333% | 118.000% |

| 4 | 69.333 | 126.667% | 125.333% | 124.000% | 122.667% | 121.333% | 120.000% | 118.667% |

| 5 | 69.417 | 127.333% | 126.000% | 124.667% | 123.333% | 122.000% | 120.667% | 119.333% |

| 6 | 69.500 | 128.000% | 126.667% | 125.333% | 124.000% | 122.667% | 121.333% | 120.000% |

| 7 | 69.583 | 128.667% | 127.333% | 126.000% | 124.667% | 123.333% | 122.000% | 120.667% |

| 8 | 69.667 | 129.333% | 128.000% | 126.667% | 125.333% | 124.000% | 122.667% | 121.333% |

| 9 | 69.750 | 130.000% | 128.667% | 127.333% | 126.000% | 124.667% | 123.333% | 122.000% |

| 10 | 69.833 | 130.667% | 129.333% | 128.000% | 126.667% | 125.333% | 124.000% | 122.667% |

| 11 | 69.917 | 131.333% | 130.000% | 128.667% | 127.333% | 126.000% | 124.667% | 123.333% |

| 70.000 | 132.000% | 130.667% | 129.333% | 128.000% | 126.667% | 125.333% | 124.000% |

SUPPLEMENTAL MATERIAL

When a retiree creates an account with the SS agency, the agency provides the dollar amount of benefits at “Full Retirement Age.”

The Full Retirement Age depends on the year the person was born.

| 1943-1954 | 66 |

| 1955 | 66 + 2 m |

| 1956 | 66 + 4 m |

| 1957 | 66 + 6 m |

| 1958 | 66 + 8 m |

| 1959 | 66 + 10 m |

| 1960 - | 67 |

At FRA, people receive 100% of their benefits. In the case of early retirement, a benefit is reduced 5/9 of one percent for each month before FRA, up to 36 months. If the number of months exceeds 36, then the benefit is further reduced 5/12 of one percent per month. After FRA, a benefit is increased by 2/3 of 1% per month or 8% annually. As the date of birth is entered in Step 1, and the age to start collecting SS in Step 2, the tool calculates the monthly dollar amount of the Social Security benefit.

Table 1

Table 1 shows the percentage by which it is necessary to multiply the FRA to get the Social Security benefit per month. The percentage depends on the year that a person was born and the age at which he/she can collect Social Security benefits. At FRA, people receive 100% of their benefits.

Table 2

When a worker files for retirement benefits, the worker's spouse may be eligible for a benefit called the Spousal Benefit, which is based on the worker's earnings. At full retirement age, the Spousal Benefit is 50% of the worker’s earnings. If the spouse begins receiving benefits before "normal (or full) retirement age," the spouse will receive a reduced benefit that is calculated using the factors in Table 2,

Table 3

Table 3 is the same as Table 1 but the factors are calculated by months instead of by years.

Source of Tables 1, 2, and 3: Author calculations based on the above IRS guidelines.

INTRODUCTION

A buoy allows boats and ships to navigate safely.

Red, Right, Returning means that the position of the red buoy should be on the right side of the ship (starboard) when returning from sea.

Photograph of Cartagena Harbor, with permission of Martha Del Valle.

In the same way that a buoy helps boats and ships to navigate safely in and out of the harbor, carefully considering and weighing various retirement options can help a retiree navigate to a safe and comfortable retirement. During navigation, a ship changes course many times and the Captain must always check to be sure that the ship is on a safe course. That is why he constantly asks his navigation officer, "Where are we?". So, check your retirement plans by asking your certified financial planner (CFP), at least every six months, "Where are we?".

What to Look for in Your Portfolio and in this Tool

Dr. Wade Pfau stated in his book, How Much Can I Spend in Retirement, that, in general, there are four retirement objectives: that you should look for:

- Lifestyle – Am I withdrawing enough money from my Portfolio to maintain my standard of living?

- Longevity – Based on my Portfolio withdrawal strategy, how many years will my savings last?

- Legacy or Bequest – Will I be able to leave some money to my children when my spouse and I die?

- Liquidity – Will I be able to quickly convert my assets into cash, without losing its value, to pay for my regular living and emergency expenses?

All the inputs that you enter, in Steps 1 through 9, modify these points. If after entering your data, the objectives are met, excellent. If not, then the “What-ifs” begin to accomplish your financial goals. On the navigation bar, click on “Charts” and keep your eyes on Figures 1 and 2 all the time.

How to Use this Tool

There are only 9 Steps for entering basic information about your retirement. Steps 1 through 4 refers to your current financial situation. Steps 5 to 9 refer to decisions about your retirement. There are some unlocked boxes where you can enter information, and some other boxes, locked, where the tool does instant calculations and lets you know the results with respect to inputs that you entered in that step. Use Tab to move from one box to another.

If you are a numbers person, click on Table, start entering information, Steps 1 through 9, and see how the table changes as you enter the information. If you are a visual person, then click on Charts, enter the information, Steps 1 through 9, and see how the charts change.

There is no need to read any of the material on the different web pages in order to use this tool. But if after using the tool, you are interested in knowing more about retirement, Social Security Benefits, Required Minimum Distributions, and taxes after retirement, read the supplemental material provided in several places in this tool and get a better understanding of how the tool comes up with the results it produces, as well as the significance of those results.

After entering all required information in Steps 1 – 9, you can print a report of your portfolio analysis including graphs, tables, snapshots, and some retirement and financial information. Select Report in the navigation bar and click on “Print” at the end of the page.

Thanks for using checkyourretirment.com.

Synopsis

The goal of several retirement tools is to determine if your savings will last for a specific number of years, regardless of whether your withdrawals will be enough to maintain your standard of living during retirement, i.e., pay for the spending you are accustomed to.

According to Nobel Laureate Robert C. Merton, PhD, “A good retirement goal is to sustain the standard of living enjoyed in the latter part of work life.” He goes on to say, “Then you have to convert that goal to a financial goal, and that conversion essentially was to say that standard of living is probably best defined by income, rather than accumulation of wealth.” The total income at retirement comes mainly from Social Security, pensions, annuities, and money that you are able to withdraw from your portfolio.

Standard of living is the level of consumption of an individual or group. This tool’s main perspective is to look at your portfolio from the point of view of your Standard of Living Risk. Standard of Living Risk (SLR) is the risk that the current or a specified acceptable lifestyle may not be sustainable.

In the tool, you select one of the seven available withdrawal strategies and then on one of the charts, you can check to see if the Total Money Available for Spending will be enough to cover your retirement spending, also called in this tool Standard of Living. If the money is enough, then there is no Standard of Living Risk that year.

If you are not interested in how all the calculations are done and all the different possible strategies, just enter your information and use the default strategies.

- Type of Retirement Spending Strategy – Select Constant Spending + Inflation. The current spending increases over the years by the rate of inflation, but in today's dollars, the amount is the same.

- Type of Portfolio Withdrawal – Select Pre-Retirement Spending. The tool calculates how much money is required to withdraw from your savings to pay for your inflation-adjusted spending (standard of living) plus taxes by calculating the following:

Portfolio Withdrawals = Expenses – Social Security – Pensions - Annuities

You withdraw money from your portfolio as you need to complement your retirement income to be able to sustain the standard of living that you want.

Remember that when you look at the charts and graphs, you are looking at them from Spouse 1’s timeline based on his/her birthday dates.

No registration or personal data about the user is required to use the tool. Inputs are saved only for the current session and then erased after the web browser is closed. However, it is possible to print a report or save it in PDF format, with all the information entered, including the financial results. Section 2 of the Report, “Assumptions (Steps 1 – 9),” shows all the inputs that the user entered.

When information is entered, the tool updates the chart, Portfolio Value over Life Cycle. Once you have entered the information, there are many ways to play, "What-ifs." Change the starting age to collect Social Security benefits; or, for example, reduce or increase your current expenses. You can also do a Sanity Check on your investments' rate of return. The portfolio will increase at a certain rate based on the type of investment selected. The Sanity Check is for you to say, for example, “I believe that future earnings will be 2% lower or 3% higher.”

When making these “What-if” changes, the idea is that either there will not be any money left when you die, or, there will be some money left for your survivors. When using the different types of withdrawal strategies, look at the chart, Retirees Base Wealth Withdrawals over Life Cycle and check that the Total Money Available for Spending is higher or the same as the Retirement Spending. If not, modify your withdrawal strategy or your expenses.

According to the US 2018 Life Table for the total population, in the United States in 2015, at 66, the remaining life expectancy of a single male is 17.4 years; 19.95 years for a single female; 24.48 years for a male-female couple; 23.26 years for a female-female couple; and 22.03 years for a male-male couple.

The results of this tool are not intended to be investment advice.

For comments and suggestions, you can send me an email at m.mogollon@checkyourretirement.com.

Manuel Mogollon, Tool Developer and Web Designer

Shabeer Pullambalavan, Software Development Engineer and Programmer

Sandra Mogollon, Editor

July 2016

Copyright

Copyright Manuel Mogollon 2011. Permission is granted to print tables and information from checkyourretirement.com provided it that it is duplicated in its entirety and appropriate credit is given to Check Your Retirement.

Software Versions

|

Date |

Version |

Comment |

|

12/20/2016 |

V1.0 |

Tool went live. |

|

05/10/2017 |

V1.5 |

Added “When to Start Social Security” calculator. |

|

08/29/2017 |

V1.7 |

Added capability to generate and print a “Report.” |

|

09/14/2017 |

V1.8 |

Included a “Run Demo” for the tool to automatically enter some financial data for the user to play “what-if” and learn how to use the tool. |

|

09/27/2017 |

V1.9 |

Included a video tutorial on how to use the tool. |

|

09/30/2017 |

V2.0 |

Added a Monte Carlo simulation. |

|

12/26/2017 |

V2.1 |

Added a chart showing the Normalized Savings, Probability of Survival, and Probability of Secure Retirement. The probability of Secure Retirement uses the GammaDist Equation 2, page 4, from Moshe Milevsky’s “A Gentle Introduction to the Calculus of Retirement Income: What is Your Retirement RisQuotient?” |

|

01/15/2018 |

V2.2 |

Updated the tool with the following: (1)New Tax Brackets (2018) for Single and Married Couple Filing Jointly; (2)Rate of return and volatility for the Conservative, Moderate, and Aggressive portfolios as calculated at PortfolioVisualizer.com for 2008-2017; (3) The average 2008-2017 inflation used by the tool for calculating Social Security and retirement spending. |

|

02/05/2018 |

V2.3 |

Corrected formulas to calculate Blanchet Retirement Spending Smile. |

|

02/10/2018 |

V2.4 |

Changed formulas to calculate taxes after the IRS canceled a tax exemption for people over 65. |

|

03/14/2018 |

V2.5 |

In “Charts” added Figure 5, Longevity & Remaining Life Expectancy Statistics for 65-Year-Olds. |

|

11/15/2018 |

V2.6 |

Included in “Portfolio Analysis” / “Longevity”, an “Individual and Joint Longevity” calculator, which shows expectancy-life statistics, how many more years people are going to live, as an individual or when a couple. Uses the Society of Actuaries 2012 Individual Annuity Mortality with projected improvements for a 2018 start date. |

|

04/01/2019 |

V3.1 |

Updated the tool with the following: (1)New Tax Brackets (2019) for Single and Married Couple Filing Jointly; (2)Rate of return and volatility for the Conservative, Moderate, and Aggressive portfolios as calculated at PortfolioVisualizer.com for 2009-2018; (3) The average 2009-2018 inflation used by the tool for calculating Social Security and retirement spending. |

|

08/05/2019 |

V3.2 |

Updated the tool by adding a new type of portfolio withdrawal strategy, “Consumption Smoothing.” Now the tool, Check Your Retirement, has eight withdrawal retirement strategies: |

|

03/08/2020 |

V4.1 |

Updated the tool with the following: (1)New Tax Brackets (2020) for Single and Married Couple Filing Jointly, as well as the Long Term Capital Gain Tax Brackets; (2)Income tax exemptions; (3)Rate of return and volatility for the Conservative, Moderate, and Aggressive portfolios as calculated at PortfolioVisualizer.com for 5-year, Jan 2015 – Dec 2019; (4) The average 20010-2019 inflation used by the tool for calculating Social Security and retirement spending; (5) New age, 72, for starting RMDs, |

|

03/14/2021 |

V4.2 |

Updated the tool with the following: (1)New Tax Brackets (2021) for Single and Married Couple Filing Jointly, as well as the Long Term Capital Gain Tax Brackets; (2)Income tax exemptions; (3)Rate of return and volatility for the Conservative, Moderate, and Aggressive portfolios as calculated at PortfolioVisualizer.com for 5-year, Jan 2016 – Dec 2020; (4) The average 2011-2020 inflation used by the tool for calculating Social Security and retirement spending; (5) New age, 72, for starting RMDs, |

A printed user manual for CheckYourRetirement.com is available here.

Update Date & Software Version

-

03/14/2021 V4.2 Updated the tool with the following: (1)New Tax Brackets (2020) for Single and Married Couple Filing Jointly, as well as the Long Term Capital Gain Tax Brackets; (2)Income tax exemptions; (3)Rate of return and volatility for the Conservative, Moderate, and Aggressive portfolios as calculated at PortfolioVisualizer.com for 5-year, Jan 2015 – Dec 2019; (4) The average 20010-2019 inflation used by the tool for calculating Social Security and retirement spending; (5) New age, 72, for starting RMDs,

-

02/15/2024 V4.3 Updated the tool with the following: (1)New Tax Brackets (2023) for Single and Married Couple Filing Jointly, as well as the Long Term Capital Gain Tax Brackets; (2)Income tax exemptions; (3)Rate of return and volatility for the Conservative, Moderate, and Aggressive portfolios as calculated at PortfolioVisualizer.com for 5-year, Jan 2019 – Dec 2023; (4) The average 2014-2023 inflation used by the tool for calculating Social Security and retirement spending.

INFORMATION ABOUT RETIREMENT AND THIS TOOL

If you are planning your retirement and you want a simple tool to make some basic calculations, this is your instrument. You don’t need to register or provide personal information. Just use the tool and, then, if you think that you would benefit from professional services, go ahead and hire a certified financial planner (CFP) to help you with planning your retirement. This is not the same as getting help with your investments (Registered Investment Adviser) or with your taxes (Tax Advisor or Tax Consultant).

In Lewis Carroll’s book, Alice in Wonderland, Alice asked the Cat:

“Would you tell me, please, which way I ought to go from here?"

"That depends a good deal on where you want to get to."

"I don't much care where –"

"Then it doesn't matter which way you go.”

We can create an analogy between this conversation and that between an investor and a Financial Planner in which the investor asks the Financial Planner:

“How much money can I spend in retirement?”

“What are your goals for retirement?”

“I don’t have any.”

“Then, you can spend your pre-retirement money any way you want.”

This analogy helps us see that it is not possible to determine how much money you can spend in your retirement unless you know your retirement objectives and goals. Dr. Wade Pfau stated in his book, How Much Can I Spend in Retirement, that, in general, there are four retirement objectives:

- Lifestyle – Keeping the same standard of living that you currently have before retirement or maintaining a certain level of standard of living through retirement.

- Longevity – Making retirement savings last to a certain age.

- Legacy or Bequest – The real value of assets at death, considering that you could die in any year according to the mortality table probabilities.

- Liquidity – Preserving the ability to quickly convert an asset into cash, without losing its value, to pay for regular living and emergency expenses.

These four objectives are interrelated and for most people’s savings, there is a tradeoff between these objectives, so it is necessary to determine the value of each objective to be able to balance them.

The focus of this tool centers on the users’ main goal revolving around their lifestyle spending. The lifestyle spending or standard of living is nothing more than the Retirement Spending (Step 7) in this tool. Once users enter their financial information, they can check the Longevity and Legacy objectives. If the objectives are met, excellent. If not, then the “What-ifs” begin.

The factors that control wealth after retirement, and by extension, the retirement objectives, include the following:

- How much money people have in savings when they retire? See Step 3 – Savings before Retirement, and Step 4 – Current Savings.

- How are savings invested? This really means, at what interest rate is it forecast that savings will grow? See Step 6 – Types of Investment.

- How much money is withdrawn from the portfolio? See Step 7 – Retirement Spending.

- What are the statistics regarding lifetime expectancy? See Figure 4 in Charts, Gompertz - Makeham Probability of Survival (tPx).

These are the factors that users need to play within the tool to achieve their three retirement objectives.

There are many articles about withdrawing money from your portfolio and several of those strategies are used in this tool and you can select one of them in Step 9 – Type of Portfolio Withdraw Strategy. After making a selection, check to make sure it meets your objectives.

The tool also provides answers about retirement results from different perspectives. For example:

-

Snapshot – Provides detail portfolio information at particular ages, which can be used to verify the state of the user’s portfolio at specific ages.

-

When to start Social Security? – The tool answers the following question: “What happens to my portfolio value over time if I change my starting Social Security age? For example, would the year-end balance of my portfolio at 75 years of age go up or down if I start Social Security at 70 instead of 66?

-

Monte Carlo Simulation – A Monte Carlo simulation analyzes the likelihood of a portfolio being successful by randomizing certain factors and checking the annual result at certain points called percentiles. In this tool, the interest per year changes at random (using the invert of the normal distribution). Then, the simulation is run 500 times each year and the percentiles, 25%, 50%, and 75% are plotted on a graph.

-

Probability of Retirement Ruin – It is the probability that a fixed spending plan will deplete a retirement nest egg prior to the end of the lifecycle and it is expressed by calculating the Gamma Distribution Function. In Figure 4, the tool shows the Probability of Secure Retirement, which is equal to (1 – Probability of Retirement Ruin).

Money Required To Retire

If you do some research you will find that, in "101 Ways to Build Wealth," Money Magazine article, May 2014, you will need the following:

7.3 x your salary by 55 to retire at 65 and replace 70% of your income.

7.7 x your salary by 55 to retire at 68 and replace 80% of your income.

6.4 x your salary by 55 to retire at 68 and replace 70% of your income.

Or, according to Fidelity, you will need the following level of savings so you won't outlive your savings during 25 years of retirement:

|

By Age

|

You Should Have This Much of Your Salary Saved...

|

By Age

|

You Should Have This Much of Your Salary Saved...

|

|

30

|

1x

|

50

|

6x

|

|

35

|

2x

|

55

|

7x

|

|

40

|

3x

|

60

|

8x

|

|

45

|

4x

|

67

|

10x

|

Again, per Nobel laureate Robert C. Merton, PhD., there are only four ways to improve the chances for achieving a good retirement:

- Save more for retirement and lower lifetime consumption level

- Work longer before retiring

- Take more risk and be prepared for the consequences if the risk is realized

- Improve the income benefits from the assets that are already available

- Annuities

- Reverse mortgage

- Goal-based investment strategies

- Redesign employer contribution schedule, for fixed contribution cost

How To Invest Your Savings at Retirement Age

Most people don’t need to time the market, what they need is a professional planner who would invest their money in a simple, well-diversified portfolio, with a low-cost, no-load index that does not require market timing. That type of investment is called the “Lazy Portfolio”. If you want to do one yourself, go to https://www.portfoliovisualizer.com, choose one of the lazy portfolios, and it will give you the ticker name, percentage allocation, and its performance over a certain period of time.

Portfolio Withdrawal

There are many portfolio withdrawal strategies and many papers that have been written about them. Some of these are included in this tool. At the end, the portfolio is calculated for every year as follows:

Balance at the End of the Year = Balance at the Beginning of the Year + Interest - Withdrawals

Age and Mortality

What is your remaining lifetime? If you know that you will die before 75, then you can spend more of your retirement, but what about if you live to 95? Maybe you will need to spend less.

That is all that counts!

That is all that counts!

You may ask, what about the income that I have after retirement, such as Social Security, pensions, annuities; also, what about my expenses during retirement, don’t they count? Well, one of the withdrawal strategies, Pre-Retirement Spending, takes into account these factors by calculating the following:

Portfolio Withdrawals = Expenses + Taxes Social Security Pensions - Annuities

You withdraw money from your portfolio as you need to complement your retirement income to be able to sustain the standard of living that you want.

INPUTS

There are only 9 Steps for entering basic information about your retirement. Steps 1 through 4 refer to your current financial situation. Steps 5 to 9 refer to decisions about your retirement. There are some unlocked boxes where you can enter information, and some other boxes, locked, where the tool does instant calculations and lets you know the results with respect to inputs that you entered in that step. Use Tab to move from one box to another.

Step 1 Date of Birth and Retirement Age

In this tool, the retirement age is the age at which you stop working, which is different from the age at which you start collecting Social Security benefits. The Social Security agency uses the word "retirement" as the age at which you start receiving Social Security benefits.

Step 2 Social Security Benefits

In this step, enter the age at which you and your spouse will start collecting Social Security benefits, as well as the Social Security benefits at FRA (full retirement age).

The Social Security full retirement age (FRA) depends on the year that a person was born. At FRA, people receive 100% of their benefits. In the case of early retirement, a benefit is reduced 5/9 of one percent for each month before full retirement age, up to 36 months. If the number of months exceeds 36, then the benefit is further reduced 5/12 of one percent per month. After full retirement age, a benefit is increased by 2/3 of 1% per month or 8% annually. As the date of birth and retirement age are entered in Step 1, the tool calculates the monthly dollar amount of the Social Security benefit.

When a worker files for retirement benefits, the worker's spouse may be eligible for a benefit called Spousal Benefit, based on the worker's earnings. At full retirement age, the Spousal Benefit is 50% of the worker’s earnings. If the spouse begins receiving benefits before "normal (or full) retirement age," the spouse will receive a reduced spousal benefit. See Table 2, in the SS Benefits web page.

But, if the spouse is also eligible for a retirement benefit based on his or her own earnings, Social Security pays the higher of the two possible benefits, his/her own earnings or the Spousal Benefit. This amount appears in Spouse 2 Social Security per Month.

If the retirement age is lower than the age when the person starts collecting Social Security benefits, then the Social Security value in the tool is $0.00.

The Full Retirement Age depends on the year the person was born

|

In 1943 - 1954

|

66

|

|

In 1955

|

66 + 2 Months

|

|

In 1956

|

66 + 4 Months

|

|

In 1957

|

66 + 6 Months

|

|

In 1958

|

66 + 8 Months

|

|

In 1959

|

66 + 10 Months

|

|

In 1960 -

|

67

|

When a person creates an account at the SS agency, the agency provides the dollar amount of the benefits at "Full Retirement Age." Using Table 1 on the SS Benefits webpage, the tool calculates the percentage of the Full Retirement Age Benefit (FRA) that would be received based on the user’s birth year, and the age when the retiree would like to start receiving the benefit, anywhere from age 62 to 70. Then, the tool multiplies that percentage by the FRA entered by the user, and that is the Social Security benefit that would be received per month.

Source of Tables 1, 2, and 3 on the Social Security webpage in this tool: Author calculations based on above IRS guidelines.

Step 3 Savings before Retirement

When users are saving from their salaries, the total saving at any future time is calculated as a constant periodic investment at a constant interest rate where the periodic investment is per month. Then, these savings are added to the Portfolio (Non-IRA and IRA accounts) to calculate the Ending Balance. The value stops showing when the person retires.

The future value of these savings is calculated using the following formula:

Where:

FVA = Future value of the annuity - savings

R = Periodic payment in annuity savings per month

I = is the interest rate per month

N = Number of months

FVA = Future value of the annuity - savings

R = Periodic payment in annuity savings per month

I = is the interest rate per month

N = Number of months

Step 4 Current Savings

Current Savings is divided into two groups, Taxable (Non-IRA) and Tax-Deferred IRA accounts.

Taxable accounts, also called non-qualified or non-IRA retirement accounts, are regular accounts in which income taxes have already been paid prior to the investment, and taxes are paid only on growth, earnings and withdrawals during the year that they are received.

Taxable accounts, also called non-qualified or non-IRA retirement accounts, are regular accounts in which income taxes have already been paid prior to the investment, and taxes are paid only on growth, earnings and withdrawals during the year that they are received.

Tax-Deferred IRA accounts, also called qualified investment accounts, are the traditional IRA accounts, 401K, 403(b)(7) in which you don’t pay income tax (tax-deferred) until you make a withdrawal. For tax purposes, traditional IRA distributions are considered ordinary income. The amount of the IRA distribution is added to other sources of income to determine the adjusted gross income; taxes are paid according to the person’s tax bracket.

A person can’t use a Roth IRA contribution as a deduction on a tax return, but the required minimum distribution (RMDs) doesn’t have to be taken during his/her lifetime. So, if Roth IRA accounts are part of the portfolio, include them as taxable accounts in the tool. Remember that there is a 10% federal penalty tax on withdrawals taken before age 59½. https://investor.vanguard.com/ira/roth-vs-traditional-ira

The tool uses IRA Minimum Required Distribution percentages to determine the amount by which each IRA account needs to be reduced after age 70 to calculate taxes. Taxes increase annual total expenses.

The portfolio current savings future value, which increases at a constant interest, is calculated using the following formula:

![]()

Where:

FV is the future value of the current portfolio account

PV is the present value of the investment portfolio account

i is the interest rate per year

is the number of years, from today’s year to retirement

FV is the future value of the current portfolio account

PV is the present value of the investment portfolio account

i is the interest rate per year

is the number of years, from today’s year to retirement

Step 5 Other Incomes After Retirement

In this step, users can enter any pension plan, annuity, or income that will be received per month after retirement. The tool adds the annual amounts which are used in all calculations.

Step 6 Type of Investments

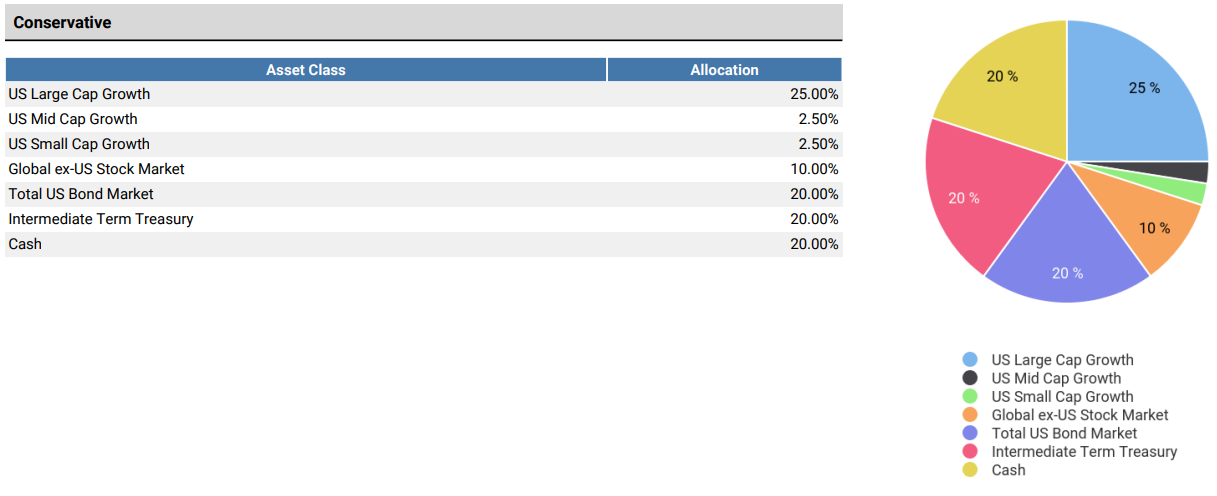

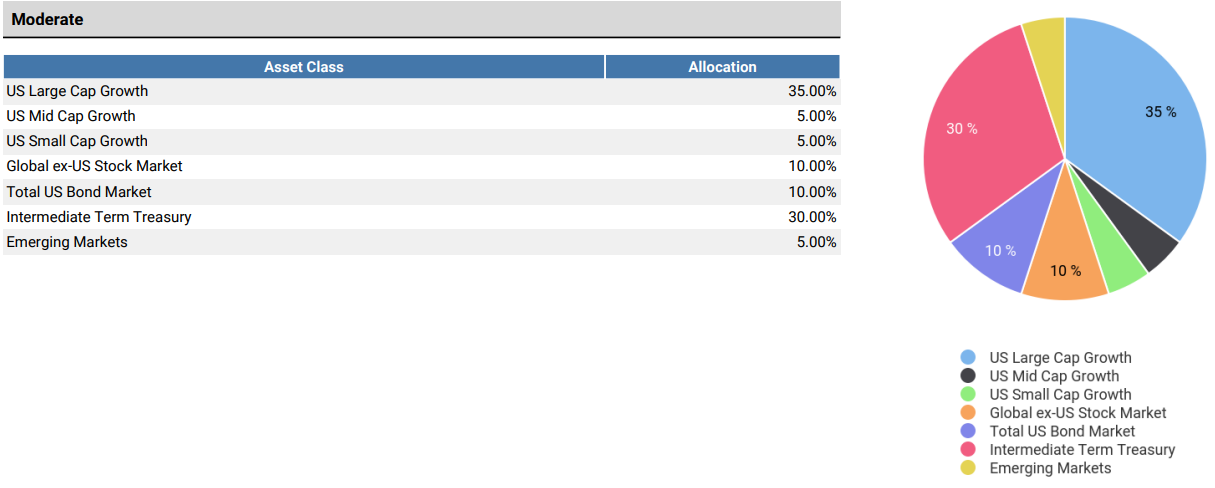

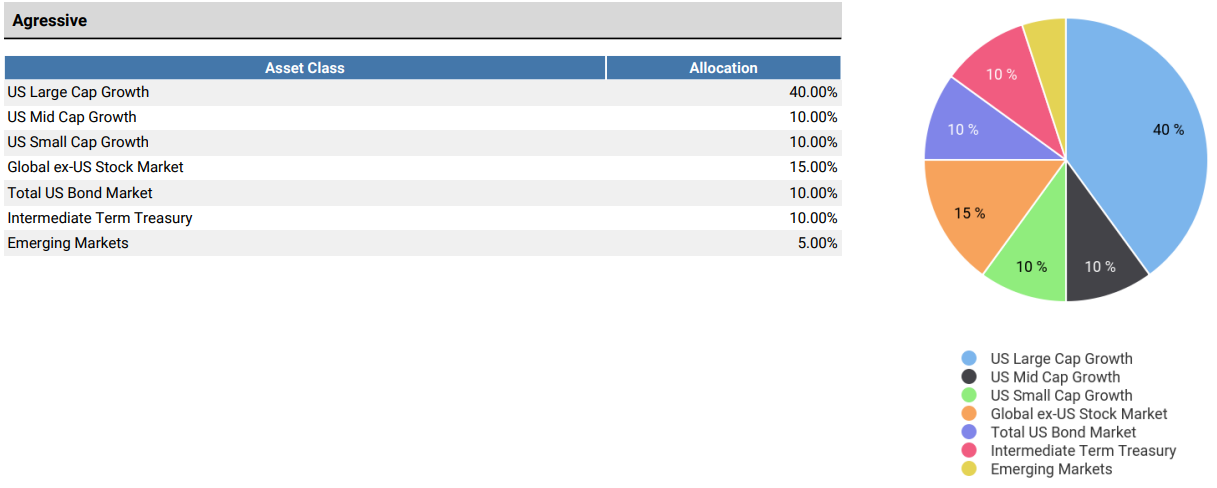

The tool provides three types of investment strategies: Conservative, Moderate, and Aggressive, based on Portfolio Investment Strategies (From Money Magazine, November 2011).

- Conservative: 40% stocks, 40% bonds, 20% Cash;

- Moderate: 60% stocks, 40% bonds;

- Aggressive: 80% stocks, 20% bonds.

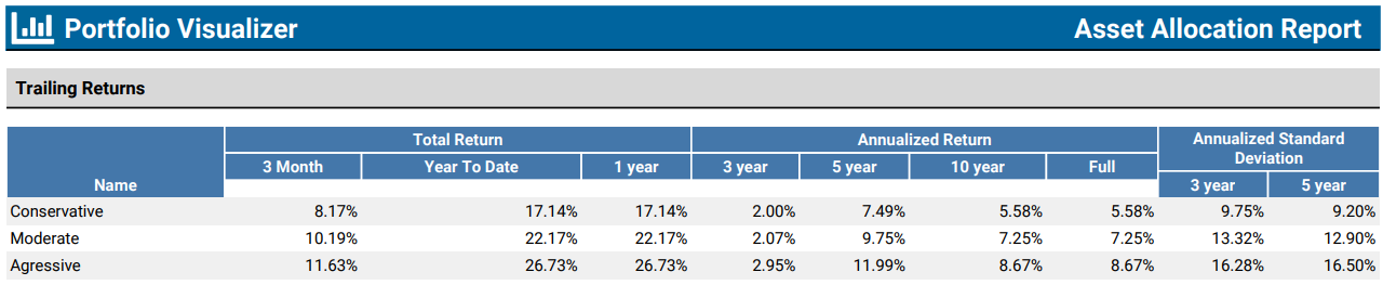

Then, a tool at Portfolio Visualizer, https://www.portfoliovisualizer.com/backtest-asset-class-allocation, is used to determine the 10-year Compound Annual Growth Rate (CAGR), as well as the Standard Deviation -Risk Volatility, for these investment strategies. The rate of return and volatility selection apply for both before and after retirement.

The tool values are updated every year, as an example, the charts below show the Portfolio Visualizer results of calculating the 5-year CAGR between January 2019 through December 2023 and 10-year CAGR between 2014-2023. The Standard Deviation, Risk Volatility, for these Conservative, Moderate and Aggressive investment strategies are also calculated.

Step 7 Inflation Adjusted Pre-Retirement Spending at Retirement Age Spending

By entering your current, pre-retirement annual expenses in the tool, it can calculate the future value of those expenses at retirement age based on the cost of living. When you select “Pre-Retirement Spending” as the withdrawal strategy, the tool calculates how much money is required to withdraw from your savings to pay for your inflation-adjusted spending, also called Standard of Living at retirement.

Step 8 Type of Spending over Lifetime

A common approach to estimating the total amount of spending over retirement is to say, “I would like to maintain a lifestyle during retirement similar to the one I have right now.” Or, to put it in another way, how much of my lifestyle do I want to keep? Once you decide on a figure, you enter your pre-retirement expenses in Step 8 and the tool calculates your spending based on inflation.

There are several articles that have been written indicating that in reality, spending over retirement does not remain the same, or increase each year by inflation or by some otherwise static percentage. In this tool, we use the findings of David Blanchett, Head of Retirement Research at Morningstar Investment Management company in his paper, “Estimating the True Cost of Retirement,” to determine spending during retirement. In his analysis, David Blanchett and his associates created an equation to determine the change in real annual spending as a function of age and the after-tax total expenditure target (ExpTar), which, in this tool, is called pre-retirement expenses.

![]()

Where:

ΔAS = Change in real annual spending

ExpTar = After-tax total expenditure target of a retiree

ΔAS = Change in real annual spending

ExpTar = After-tax total expenditure target of a retiree